It is too late to apply under the CARES Act Paycheck Protection Program, but another chance to borrow has been rolled out under new legislation.

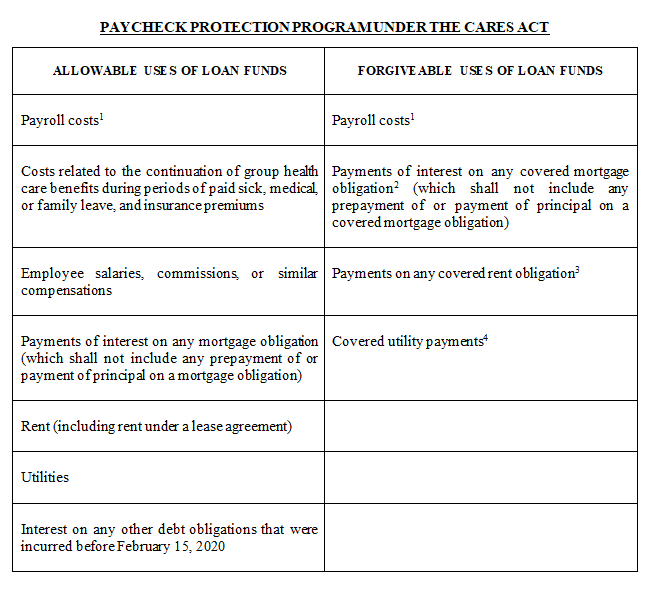

Learn More About PPP Second DrawIf you look at the chart below, you will see that all forgivable uses are allowable, but not all allowable uses are forgivable. The allowable use rules with respect to PPP funds are in a completely separate section of the CARES Act than the forgiveness rules. Thus, allowable uses and forgivable uses should be viewed as (and are) independent rules.

Remember

- The allowable use rules apply at all times, and;

- the forgivable use rules apply during the 8 week period following the date the loan is received.

- Only up to 25% of the PPP loan proceeds used for rent, utilities, and mortgage interest is forgivable.

Though a borrower may have funds left over after the forgiveness period ends, such borrower is still limited on how it can use those funds.

Please contact your Carlile Patchen & Murphy LLP attorney, if you have any questions or need further guidance.

1 “Payroll costs”:

- The sum of payments of any compensation with respect to employees that is a—

(a) salary, wage, commission, or similar compensation;

(b) payment of cash tip or equivalent;

(c) payment for vacation, parental, family, medical, or sick leave;

(d) allowance for dismissal or separation;

(e) payment required for the provisions of group health care benefits, including insurance premiums;

(f) payment of any retirement benefit; or

(g) payment of State or local tax assessed on the compensation of employees.

- The sum of payments of any compensation to or income of a sole proprietor or independent contractor that is a wage, commission, income, net earnings from self-employment, or similar compensation and that is in an amount that is not more than $100,000 in 1 year, as prorated for the covered period.

- Does NOT include—

(a) the compensation of an individual employee in excess of an annual salary of $100,000, as prorated for the covered period;

(b) Federal payroll taxes;

(c) any compensation of an employee whose principal place of residence is outside of the United States;

(d) qualified sick leave wages for which a credit is allowed under section 7001 of the Families First Coronavirus Response Act (FFCRA); or

(e) qualified family leave wages for which a credit is allowed under section 7003 of the FFCRA.

2 “Covered mortgage obligation’’ means any indebtedness or debt instrument incurred in the ordinary course of business that—

(a) is a liability of the borrower;

(b) is a mortgage on real or personal property; and

(c) was incurred before February 15, 2020.

3 “Covered rent obligation” means rent obligated under a leasing agreement in force before February 15, 2020.

4 “Covered utility payment” means payment for a service for the distribution of electricity, gas, water, transportation, telephone, or internet access for which service began before February 15, 2020.

0 Comments